Federal Fiscal Court, 12.05.2011, VI R 42/10

In order to determine the income tax due, the taxable income (Section 2 (5) EStG) must first be calculated, to which the respective tax rate must then be applied.

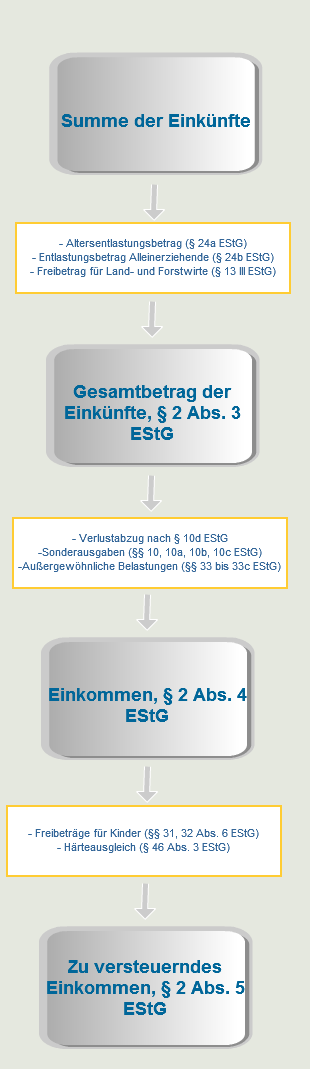

The taxable income is determined in four steps:

1) Adding up the income from the seven types of income (income from agriculture and forestry, from business, from self-employment, from employment, from capital assets, from letting and leasing and other income) gives the total income.

2) If the respective requirements are met, the old-age relief amount, the relief amount for single parents or the deduction for farmers and foresters can be deducted from this total income, resulting in the total amount of income.

3) Special expenses and extraordinary expenses can in turn be deducted from this total amount of income to arrive at the income.

4) If the allowances for children and the hardship allowance are deducted from this income if the requirements are met, the taxable income is finally calculated.

In particular, the question of whether legal costs in civil proceedings constitute deductible special expenses or extraordinary expenses has repeatedly been the subject of legal disputes.

The above-mentioned landmark decision of the Federal Fiscal Court also dealt with this subject matter.

Facts of the Case:

The plaintiffs in the above-mentioned case were husband and wife and were jointly assessed for income tax.

The plaintiff had private health insurance with an insurance company that included daily sickness benefit insurance for a daily sickness benefit after six weeks of incapacity for work.

The plaintiff was employed as a management assistant. At the beginning of 2004, the plaintiff went on sick leave.

After six weeks, the employer stopped paying his salary. The insurance company was then called in, which initially paid the contractually agreed daily sickness allowance.

At the request of the insurance company, the plaintiff was examined by a doctor in 2005.

The expert report certified that the plaintiff was not only unable to work but also unable to work.

The insurance company then took the view that the claimant's obligation to pay daily sickness benefits had ceased from the time of her incapacity to work.

Plaintiff sued her insurance company for daily sickness benefits

As the policyholder, the plaintiff then brought an action against the insurance company.

The action was aimed at establishing the continued existence of the daily sickness allowance insurance and the payment of daily sickness allowance. The claim was dismissed.

The plaintiff claimed the legal costs as income-related expenses

One year later, the plaintiffs claimed the legal costs in their income tax return as income-related expenses in the plaintiff's income from employment.

The defendant (tax office) did not agree because daily sickness benefits are regularly tax-free and the process therefore did not serve to generate taxable income.

The FA rejected the objection directed against this, in which the claimants asserted that the legal costs should be taken into account as an extraordinary burden, as unfounded in its objection decision dated 5 January 2009.

The Cologne Fiscal Court dismissed the action brought against this.

Decision of the Federal Fiscal Court

BFH ruled that the Cologne Fiscal Court had wrongly not recognised the costs as extraordinary expenses

In the above-mentioned judgement, the Federal Fiscal Court now found that the Cologne Fiscal Court had wrongly excluded the plaintiff's civil proceedings costs from deduction as extraordinary expenses and ruled against its previous case law:

According to § 33 EStG, the income tax of an applicant is reduced if the taxpayer inevitably greater expenses than the vast majority of taxpayers with the same income, assets and marital status (extraordinary burden).

According to the established case law of the Federal Fiscal Court (BFH), there is a presumption against this inevitability in the case of the costs of civil proceedings.

Such costs had previously only been considered inevitable if the event that adequately caused the payment obligation or the payment claim had also inevitably arisen.

According to the previous case law of the BFH, this is generally not the case in civil proceedings, as it is generally left to the free decision of the parties as to whether they expose themselves to a litigation (cost) risk in order to enforce or defend a civil law claim.

If the taxpayer enters into a lawsuit despite the uncertain outcome, the cause of the legal costs lies in his decision to accept the risk of legal costs in the hope of a favourable outcome for him; it would not correspond to the meaning and purpose of Section 33 EStG to relieve him of the cost burden if the risk consciously accepted in his own interest had materialised.

The BFH no longer adheres to this case law.

This is because the view that the taxpayer "voluntarily" assumes the risk of legal costs fails to recognise that disputed claims can regularly only be enforced or defended against in court due to the state's monopoly on the use of force, which serves to realise domestic peace.

This follows from the principle of the rule of law, which is generally laid down in Art. 20 para. 3 of the Basic Law (Grundgesetz - GG) and is specifically expressed in Art. 19 para. 4 GG for legal protection against acts of public authority.

It is a central aspect of the rule of law to deny the unauthorised enforcement of legal claims by force.

Instead, the parties would be referred to the courts to resolve legal disputes and conflicts of interest between citizens in a non-violent manner.

Civil litigation costs would therefore inevitably be incurred by the plaintiff and the defendant for legal reasons, irrespective of the subject matter of the civil litigation.

However, civil proceedings costs can only be taken into account as extraordinary expenses if the taxpayer did not enter into the proceedings wilfully or frivolously.

He therefore had to have entered into the process by reasonably weighing up the pros and cons, including the cost risk.

Accordingly, civil proceedings costs of the plaintiff and the defendant are not unavoidable if the intended prosecution or legal defence did not offer a reasonable prospect of success from the perspective of a reasonable third party.

Source: Federal Fiscal Court

SUBSEQUENT ADDITION: On 20 December 2011, the Federal Ministry of Finance published a BMF circular according to which the consideration of civil litigation costs as extraordinary expenses is rejected (non-application decree, Ref. no.: IV C 4 - S 2284/07/0031 :002).

Important Note: The content of this article has been prepared to the best of our knowledge and belief. However, due to the complexity and constant evolution of the subject matter, we must exclude liability and warranty. Important Notice: The content of this article has been created to the best of our knowledge and understanding. However, due to the complexity and constant changes in the subject matter, we must exclude any liability and warranty.

If you need legal advice, feel free to call us at 0221 – 80187670 or email us at info@mth-partner.de.

2 responses

According to the circular from the Federal Ministry of Finance to the supreme tax authorities of the federal states on the consideration of civil litigation costs as an extraordinary burden BFH judgement of 12 May 2011 VI R 42/10, this judgement is not applicable to the individual case decided.

MDg Jörg Kraeusel Head of Subdivision IV C